The PAR App has a deep history and a broad reach. For over two decades, earlier versions of this App have served not only its developer—the Center for Natural Lands Management—but a variety of similar or related interests within the larger conservation community. The “PAR” (Property Analysis Record) has been acquired and used by Resource Conservation Districts; private land owners; environmental consultants and other for-profit businesses; County, regional, state-wide, and national land trusts (including TNC); County governments; State natural resource agencies; universities; transportation authorities; and energy and other utility companies.

The majority of interest, and presumably use, of the PAR has been in California, but the program has been acquired by entities in other states (including Arizona, Louisiana, North Carolina, Utah, and Virginia) and used in other countries (e.g., Canada, Australia). Because there is only supportive structure for prompting a comprehensive input of data, but no default values, the PAR can be used in diverse contexts. Units of measurement, where applicable, can be presented using either the metric or imperial system.

What do these PAR preparers have in common? They all have found value in a tool that supports a comprehensive, objective, and transparent means of determining annual and perpetual costs of stewardship (or easement monitoring, enforcement, and defense) of conservation lands. When appropriately conducted, the PAR provides a permanent record of the attributes of the conservation property, the stewardship responsibilities, requirements, and assumptions, and the detailed costs. For conservation land-holding entities, the PAR product provides information that can be used for annual work plans and budgets, as well as endowment targets for fund-raising or endowment requirements for mitigation purposes. Regulatory agencies find value in the PAR in its transparency of components and consistent format, improving their ability to review cost analyses for mitigation properties to ensure permit compliance. When used in a mitigation context, the PAR can also be of value to the regulated community—providing the transparency that allows informed discussions about proposed endowment funding, as well as assurance that mitigation funds would serve the intended conservation purpose.

PAR APP NEWSLETTER

Volume 1 Issue 1

EDITORIAL

PAR APP TIP

General tips and pointers for using and navigating the App.

PAR COST ANALYSIS TIP

Information or ideas on how to approach the determination of tasks or costs to be included in your PAR.

QUESTIONS FROM PAR APP USERS

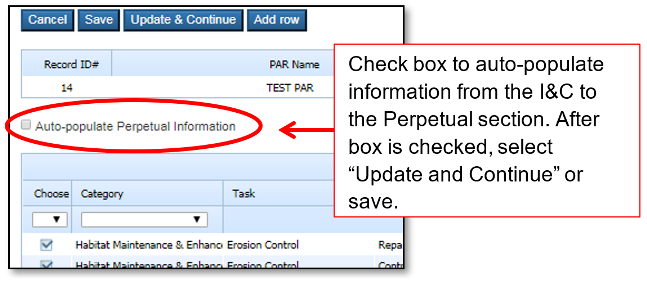

Q: In the Tasks and Cost Analysis table, after I enter some data for a labor item (i.e., position title), the labor rate automatically populates in the Initial and Capital (I&C) section. Is there some way that this can automatically populate with the same information in the Perpetual section?

A: We have made it easy to transfer the data you have entered in the I&C over to the Perpetual section: To add information from the Initial and Capital (I&C) to the Perpetual section for all selected tasks, check the “Auto-populate Perpetual Information” box and then select Save or the “Update and Continue” button. The units (“No. Units”) and cost per unit (“Cost/Unit”) will be copied over to the Perpetual section for all of your checked tasks UNLESS you have already entered values in these columns for Perpetual tasks— the values you have already entered in the Perpetual section will not be replaced when you use this function. Certain tasks that are specific to the I&C only (e.g., Account set-up) will not be auto-filled; you will also need to enter the frequency (“Freq(yrs)”) for the Perpetual tasks, as this field has no equivalent in the I&C and thus is not auto-populated.

PAR APP TEAM

Deborah L. Rogers, Ph.D.

Director of Conservation Science and Stewardship

Michelle A. Labbé, M.S.

Conservation Analyst

Romina A. Roque

IT Assistant

Questions or Comments? Contact us at parteam@cnlm.org